putilich/iStock via Getty Images

The meltdown of FTX (FTT-USD) continues to spark controversy and commentary. A recent theme in this commentary is that the FTX disaster represents a failure of centralization that decentralized finance – “DeFi” – could correct. Examples include contributions by the very smart and knowledgeable Campbell Harvey of Duke, and an OpEd in WSJ.

I agree that the failure of FTX demonstrates that the crypto business as it is, as opposed to how it is often portrayed, is highly centralized. But the FTX implosion does not demonstrate that centralization of crypto trading per se is fundamentally flawed: FTX is an example of centralization done the worst way, without any of the institutional and regulatory safeguards employed by exchanges like CME, Eurex, and ICE.

Indeed, for reasons I have laid out going back to 2018 at the latest, the crypto market was centralized for fundamental economic reasons, and it makes sense that centralization done right will prevail in crypto going forward.

The competitor for centralization advocated by Harvey and the WSJ OpEd and many others is DeFi. This utilizes the nature of blockchain technology and smart contracts to facilitate crypto trading without centralized intermediaries like exchanges.

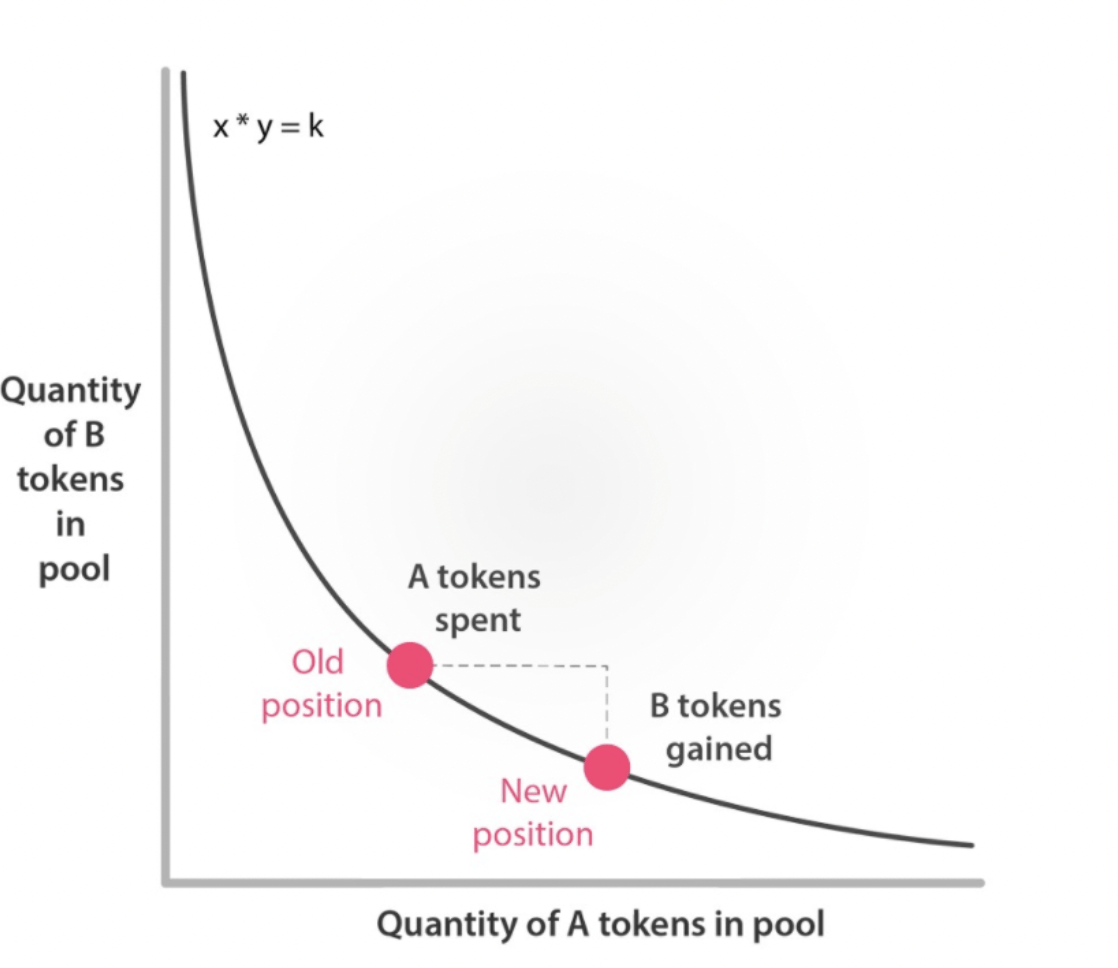

One of the exemplars of the DeFi argument is “automated market making” (“AMM”) of crypto. This article provides details, but the basic contours are easily described. Market participants contribute crypto to pools consisting of pairs of assets. For example, a pool may consist of Ether (ETH-USD) and the stablecoin Tether (USDT-USD). The relative price of the assets in the pool is determined by a formula, e.g., XETH*XUSDT=K, where K is a constant, XETH is the amount of ETH in the pool and XUSDT is the amount of Tether. If I contribute 1 unit of ETH to the pool, I am given K units of USDT, so the relative price of ETH (in terms of Tether) is K: the price of Tether (in terms of Ether) is 1/K.

Automated Market…